The sleepless nights are already costing you enough. The last thing you need is to hand over thousands of dollars to a tax relief company that promises to eradicate your IRS debt — and then disappears, stalls, or makes everything worse.

What’s the Fastest Way to Tell a Legitimate Tax Relief Firm From a Scam?

Legitimate IRS tax relief providers are distinguished by three non-negotiable credentials: licensure (Enrolled Agent, CPA, or tax attorney), transparent fee structures disclosed before engagement, and direct IRS Power of Attorney representation so you never communicate with the IRS yourself. Firms that cannot confirm all three within your first conversation should be disqualified immediately.

Key Takeaways

- Demand proof of IRS Power of Attorney representation — if a firm won’t handle IRS communication on your behalf, it isn’t a full-service tax relief provider

- Enrolled Agents, CPAs, and tax attorneys are the only three credential types legally authorized to represent you before the IRS

- Upfront fees quoted before a thorough financial review are a red flag, not a convenience

- Settlement results vary significantly based on your specific financial profile — any firm guaranteeing a specific reduction before reviewing your case is misleading you

- A firm’s track record with high-debt cases matters more than its marketing claims — ask for anonymized resolution examples with real numbers

Why Do So Many People End Up With the Wrong Tax Relief Firm?

Most people searching for IRS tax relief are not in a calm, research-ready state. They are scared. The IRS has sent a levy notice, or a lien has appeared on their credit report, or a paycheck is about to be garnished. That urgency is exactly what predatory tax relief companies exploit.

The real problem isn’t that bad firms exist — it’s that the evaluation window is compressed by fear. When you feel like you have days to act, you don’t comparison shop. You call the number from the TV ad, hear a confident voice, and sign something.

The IRS does not get emotional about collections. It just keeps moving. And firms that prey on that pressure know you’re not reading the fine print.

> The most dangerous moment in the tax relief process isn’t when the IRS sends a notice — it’s the 48 hours after, when fear overrides judgment and a bad decision gets locked in with a signature.

What’s Actually Driving the Problem — and Why It Keeps Repeating

The persistence of tax relief fraud and underperformance isn’t random. It’s structural.

The IRS tax relief industry has low barriers to marketing entry. A company can run national TV ads, build a polished website, and collect retainers without being staffed by a single licensed tax professional. The credential requirements for marketing tax relief services are essentially nonexistent — only the representation phase requires licensure.

This creates a gap. Firms sell the dream upfront and outsource (or delay) the actual IRS work until client frustration peaks or the statute of limitations shifts in the IRS’s favor.

Tax professionals commonly observe a pattern: clients arrive having already paid $3,000–$8,000 to a national firm, with no IRS correspondence filed on their behalf, and a collection clock that’s been running the entire time. The money is gone. The problem is worse.

The root cause is credential theater — the appearance of professional representation without the substance of it. Knowing how to spot that gap is the single most valuable skill a taxpayer can develop before signing anything. Understanding what you’re actually paying for in IRS tax relief — and where fees go wrong — is a critical part of that education.

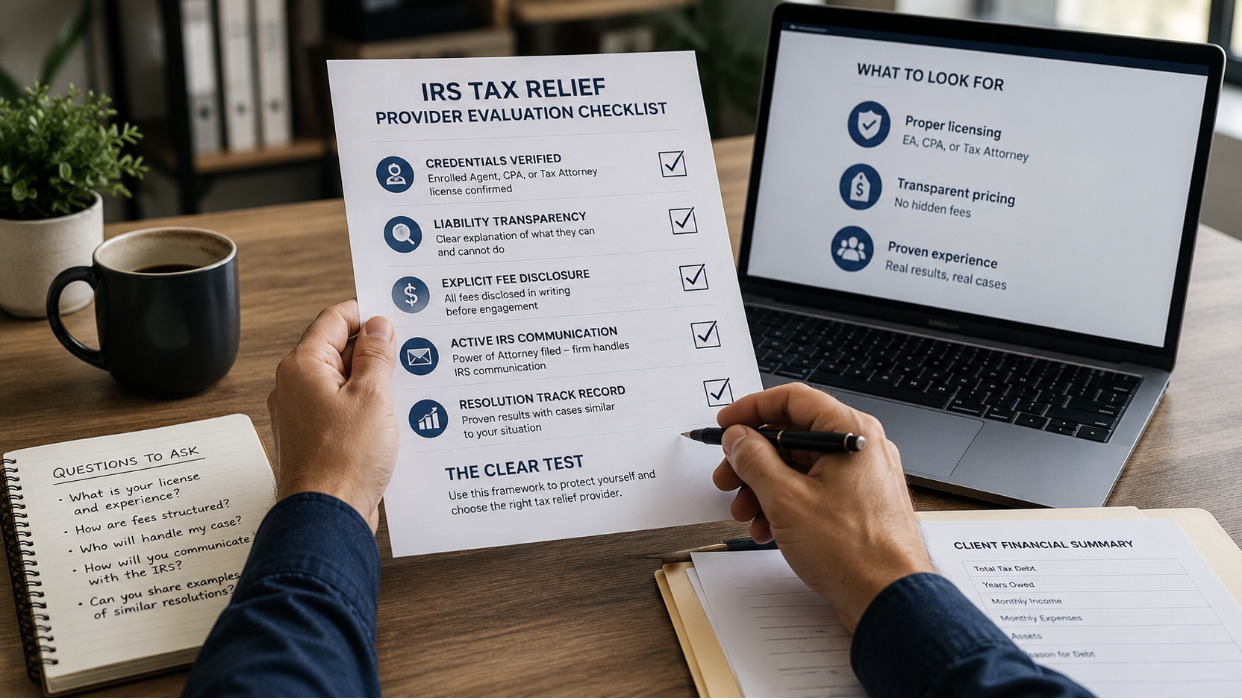

The 5-Point Provider Evaluation Framework (The CLEAR Test)

The CLEAR Test is a five-criterion evaluation framework designed to assess IRS tax relief providers before engagement. Use it when you’re comparing firms, not after you’ve already signed.

C — Credentials Verified Ask for the specific license type of the person who will handle your case. Enrolled Agent (EA), CPA, or tax attorney are the only three credentials that authorize IRS representation. A “tax consultant” or “case manager” title means nothing. Verify EA credentials at the IRS Office of Enrollment directory.

L — Liability Transparency A legitimate firm will tell you clearly what they can and cannot do for your situation. If the first call is all confidence and no caveats, that’s a sales call, not a consultation.

E — Explicit Fee Disclosure Fees should be disclosed in writing before any retainer is signed. Firms that quote fees before reviewing your transcripts, income, and assets are guessing — or inflating.

A — Active IRS Communication The firm should file IRS Form 2848 (Power of Attorney) on your behalf and handle all IRS correspondence directly. If you’re expected to call the IRS yourself or “just forward letters,” the firm is not providing full representation.

R — Resolution Track Record Ask for anonymized case examples that match your situation — similar debt amount, similar compliance history. A firm that has resolved a $72,000 liability for $5,000 can show you how. A firm that can’t cite any specific outcomes is telling you something important.

Use the CLEAR Test when: evaluating any firm before signing. Skip it when: you’ve already engaged a firm and are mid-process — at that stage, a second-opinion consultation is the better tool.

What Does Legitimate Tax Relief Actually Look Like — With Real Numbers?

Here’s what a realistic resolution process looks like, based on practitioner patterns.

A self-employed contractor with $68,000 in IRS debt — three years of unfiled returns, accruing penalties — engaged a qualified tax relief firm. The firm filed all outstanding returns first (a required step before any settlement program is available), then submitted an Offer in Compromise based on the client’s documented financial hardship. Resolution took approximately 14 months from initial engagement. The IRS accepted a settlement of $6,200.

That’s not a guarantee. That’s a real pattern of what’s possible when the right process is followed.

The mechanism that makes Offer in Compromise work isn’t negotiation skill alone — it’s financial documentation. The IRS uses a specific formula (Reasonable Collection Potential, or RCP) to calculate what it believes it can actually collect from you. A qualified practitioner builds the case that your RCP is lower than your total debt. The documentation is the argument.

> An Offer in Compromise isn’t a negotiation in the traditional sense. It’s a financial proof submission — and the quality of that proof determines the outcome more than any relationship with the IRS.

Total IRS Relief has resolved cases following exactly this pattern — including a $72,000 liability settled for $5,000 — by building the financial case correctly from the start, not by making promises.

How Do the Main Tax Relief Options Actually Compare?

| Option | Best For | Typical Timeline | Key Limitation |

| Offer in Compromise | Taxpayers with low RCP relative to debt | 12–24 months | IRS accepts fewer than half of submissions |

| Installment Agreement | Taxpayers who can pay over time | 30–90 days to establish | Does not reduce principal owed |

| Currently Not Collectible | Taxpayers with genuine financial hardship | Immediate (temporary) | IRS can resume collection when finances improve |

| Penalty Abatement | First-time compliance failures | 30–90 days | Applies to penalties only, not principal |

| Innocent Spouse Relief | Divorced/separated individuals with joint liability | 6–12 months | Requires specific qualifying circumstances |

No single option is universally best. The right resolution path depends on your specific financial profile, compliance history, and what the IRS’s own records show about your collectible assets. That’s why a transcript review — pulling your actual IRS account records — should precede any recommendation. For a direct comparison of how these tax relief options stack up against the alternatives, including when each one actually makes sense, the differences matter more than most people realize going in.

Who Is This Evaluation Process NOT For?

This framework is not useful if your IRS debt is under $10,000 and you have stable income — in that case, a standard installment agreement is usually straightforward enough to handle without full representation.

It’s also not a fit if you’re currently under criminal tax investigation. That situation requires a tax attorney with criminal defense experience, not a resolution specialist.

And if you’ve already signed with a firm and paid a retainer, the CLEAR Test won’t undo that. What it can do is help you assess whether to continue — or seek a second opinion before more time passes.

Total IRS Relief offers a consultation specifically for taxpayers who’ve already been through one failed resolution attempt and aren’t sure what happened or what to do next.

Frequently Asked Questions

How do I know if a tax relief company is actually legitimate? Check that the person representing you holds one of three credentials: Enrolled Agent, CPA, or tax attorney. Verify EA status through the IRS Office of Enrollment. Ask specifically who will file your Power of Attorney with the IRS — if the answer is vague, that’s your answer.

What does it mean when a firm says they’ll “settle my debt for pennies on the dollar”? It means they’re describing the Offer in Compromise program, which is real — but the IRS accepts fewer than half of all submissions, and qualification depends entirely on your financial profile. Any firm promising a specific reduction before reviewing your financials is making a claim they cannot support.

How long does it actually take to resolve IRS tax debt? Realistic timelines vary by resolution type. An installment agreement can be established in 30–90 days. An Offer in Compromise typically takes 12–24 months from submission to IRS decision. Unfiled returns must be filed before most resolution programs are even available, which adds time upfront.

Will a tax relief firm really handle all IRS communication so I don’t have to? A properly credentialed firm files IRS Form 2848, which grants them Power of Attorney to communicate with the IRS on your behalf. Once that’s filed, the IRS is required to work through your representative. Total IRS Relief’s clients never meet with or speak to the IRS directly — that’s a structural protection, not a marketing claim.

What happens if I have unfiled tax returns — can I still get relief? Yes, but filing compliance comes first. The IRS will not consider any settlement or payment arrangement until all required returns are filed. A qualified firm will handle the filing process as part of the overall resolution strategy, not as a separate problem.

Is it worth hiring a local firm versus a national tax relief company? National firms often use call center intake, assign cases to rotating staff, and operate at volume. A locally owned firm typically means direct access to the credentialed professional handling your case. The difference matters most in complex, high-debt situations where your specific financial details drive the outcome.

What’s the first thing I should do if I’ve already tried to resolve this on my own and it didn’t work? Request your IRS account transcripts — these show exactly what the IRS has on file, what you owe, and what collection actions are active or pending. A qualified practitioner will pull these as a first step. If a firm you’re evaluating doesn’t mention transcripts early, they’re not starting from the right place.

If You’ve Been Through This Before and It Didn’t Work, This Is for You

You already know what a failed resolution attempt feels like. The fees paid, the calls not returned, the IRS notices that kept coming anyway. That experience is exactly why the CLEAR Test exists — not to make you more skeptical of everyone, but to give you a specific, structured way to tell the difference.

Total IRS Relief was built for cases like yours — high debt, complicated history, previous attempts that went nowhere. William Sharpe, Enrolled Agent and Certified Tax Resolution Specialist, has spent 50 years in the tax industry specifically working through the situations that other firms walk away from. Much of why IRS tax relief feels harder than it should comes down to structural problems in how most firms operate — and knowing that going in changes how you choose who handles your case.

If you’re ready to stop managing this alone and have someone take over the IRS communication entirely, the next step is a direct consultation — not a sales call, not a form submission that goes to a call center. A real conversation about your specific situation, what the IRS actually has on file, and what resolution looks like for you.

Call Total IRS Relief today and tell them exactly where things stand. That’s where the process starts.

References

IRS.gov — Official source for Offer in Compromise program rules, eligibility criteria, and Reasonable Collection Potential calculation methodology

IRS Office of Enrollment — Directory for verifying Enrolled Agent credentials and licensure status

IRS Form 2848 — Power of Attorney and Declaration of Representative, governing authorized practitioner representation before the IRS

Enter your contact information to schedule your FREE one-on-one consultation. Our tax experts will get back to you as soon as possible.